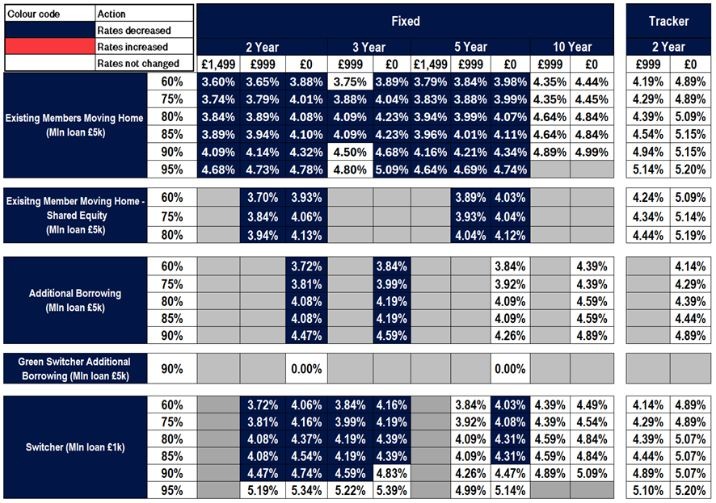

Nationwide savings rates increase: impact for savers and the wider market

Why the topic matters

The announcement of a nationwide savings rates increase has immediate relevance for savers, borrowers and households across the UK. Changes in savings rates influence household income from deposits, affect the attractiveness of saving versus spending, and can signal broader shifts in financial conditions. For banks and building societies, rate moves shape product competitiveness and customer behaviour.

Main details and context

What an increase means for savers

A rise in savings rates typically improves the return on cash held in instant-access and fixed-term accounts. Even modest uplifts can be meaningful for those with larger balances or near-term financial goals. Savers may re-evaluate where they hold cash, comparing easy-access accounts with longer fixed-term options to find the best effective yield.

Drivers behind rate changes

Savings rates are commonly influenced by market interest rates, competition among financial institutions and inflationary pressures. When central banks or market expectations push interest rates higher, banks and building societies often pass some of that through to deposit rates to attract funding. Conversely, a stable or falling rate environment can limit increases offered to customers.

Impact on borrowing and the wider market

Movements in savings rates are closely linked to borrowing costs. Higher deposit rates can coincide with higher mortgage and loan rates, affecting affordability for prospective borrowers. For lenders, balancing deposit pricing with lending margins is a key operational consideration, potentially affecting product availability and terms.

Conclusion and outlook

For individual savers, a nationwide savings rates increase presents an opportunity to secure better returns on cash, though the right choice will depend on personal goals, liquidity needs and the comparison of available products. For the broader market, such increases can indicate tighter financial conditions and a shift in the balance between saving and borrowing. Consumers should review accounts, compare rates and consider fixed-term options if they seek certainty. Observers will watch subsequent announcements from financial institutions and market indicators to judge whether the trend continues and how it will feed through into household finances and lending markets.