Mortgage rates today: what UK borrowers need to know

Introduction: why mortgage rates today matter

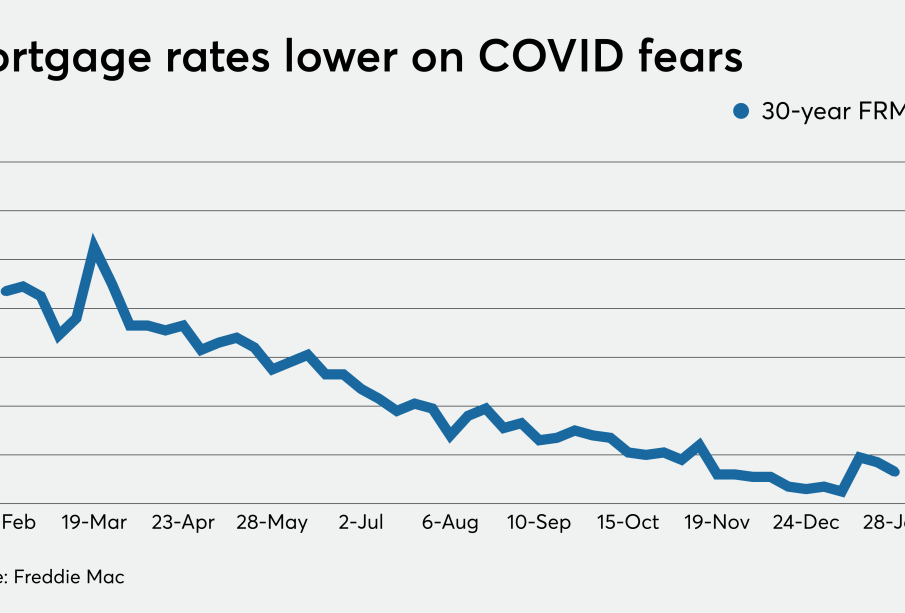

Mortgage rates today are a key consideration for anyone buying property, remortgaging or managing household budgets. Small movements in interest rates can materially affect monthly payments, borrowing costs and the wider housing market. Understanding the drivers behind current mortgage pricing and the choices available helps homeowners and prospective buyers make informed decisions.

Main developments and key factors

What determines mortgage rates today

Mortgage pricing is shaped by a mix of macroeconomic and market factors. Central bank policy—principally decisions by the Bank of England—sets the baseline for short-term interest rates and influences lenders’ borrowing costs. Inflation, wage growth and economic activity feed into expectations about future policy. In addition, wholesale funding costs, lender competition, credit risk assessments and regulatory requirements all influence the rates lenders offer to consumers.

Types of mortgages and rate sensitivity

Different mortgage products react differently to market moves. Variable and tracker mortgages move in line with base-rate changes, so borrowers on these deals feel rate shifts more quickly. Fixed-rate mortgages lock in payments for an agreed period, providing certainty but often at a premium. Longer fixed terms typically offer insulation from short-term volatility, while shorter fixes can be cheaper but riskier if rates rise.

Market sentiment and availability

Lender appetite and competition affect both pricing and product availability. When lenders are cautious—whether due to economic uncertainty or funding pressures—product ranges can narrow and rates may rise. Conversely, strong competition can lead to more attractive deals, fee-free options and enhanced mortgage service propositions.

Conclusion: implications and practical steps

Mortgage rates today reflect a complex interaction of central bank policy, inflation expectations, wholesale funding and lender strategy. For borrowers, the practical response is to assess personal circumstances, consider the trade-off between certainty and cost, and seek current offers from multiple lenders or a regulated adviser. Monitoring economic indicators and Bank of England announcements can help households time decisions, but cautious planning—including stress-testing budgets for higher rates—remains a prudent approach.