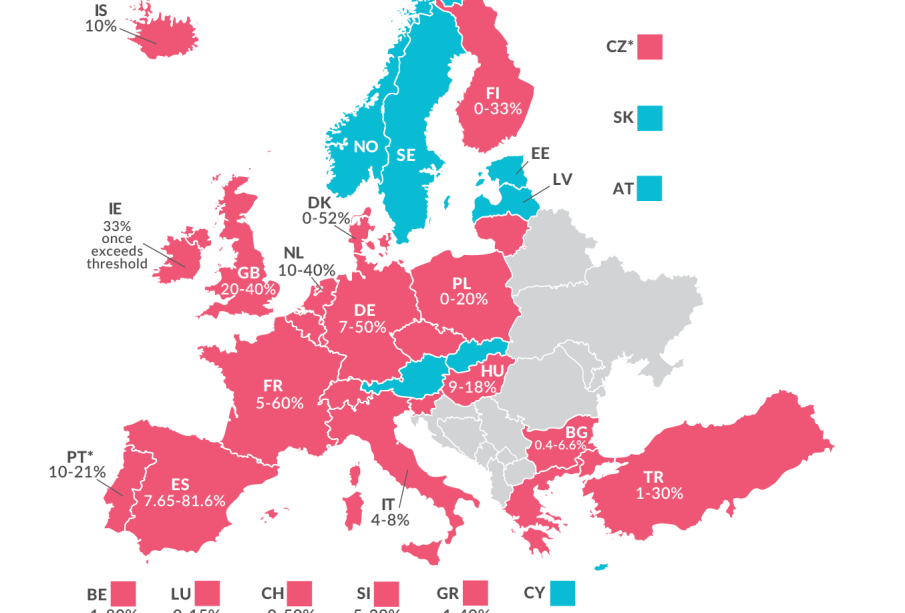

Understanding inheritance tax in the UK

Introduction

Inheritance tax is a key issue for many households and estates in the UK. It determines how much of a person’s estate is passed on to beneficiaries and how much will go to HM Revenue & Customs. Understanding inheritance tax is important for families planning transfers of wealth, for executors administering estates, and for anyone wanting to make informed decisions about gifts, property and trusts.

Main details

Thresholds and rates

An estate is liable to inheritance tax only above the nil-rate band. The standard nil-rate band is £325,000 and a residence nil-rate band of up to £175,000 can apply when a main residence is passed to direct descendants. Together, a married couple or civil partners may be able to use up to these amounts between them. Inheritance tax is charged at 40% on the value of an estate above the available allowances. If at least 10% of the net estate is left to charity, a lower rate of 36% can apply.

Exemptions and reliefs

Certain transfers are exempt. Assets left to a spouse or civil partner are generally exempt from inheritance tax. Gifts made more than seven years before death are usually exempt from tax; gifts within seven years may be subject to taper relief. There are also annual and small-gift allowances — for example a £3,000 annual exemption for gifts and exemptions for gifts to dependants or for regular maintenance. Business Property Relief and Agricultural Relief can reduce the taxable value of qualifying business or farm assets, sometimes to nil.

Practical effects and administration

Inheritance tax applies to the deceased’s estate and some lifetime transfers. Executors must report and, where due, pay tax to HMRC before probate is finalised. Trusts, joint assets and certain lifetime planning measures can complicate the calculation and timing of any liability.

Conclusion

Inheritance tax planning can materially affect what beneficiaries receive. With key allowances fixed, more estates may become liable over time unless planning is undertaken. Simple steps — such as making use of exemptions, charitable giving, careful use of lifetime gifts and seeking professional advice — can reduce unexpected bills. Individuals concerned about potential liabilities should consult a solicitor or regulated tax adviser to explore options tailored to their circumstances.